Have investment markets been NAUGHTY or NICE in 2023?

One word sums up how investment markets performed over 2023 – choppy.

Most investment sectors played peek-a-boo with investors throughout the year – at one point signalling all the signs of an imminent recession and at other times defying negative trends and outperforming expectations.

Investment markets – shares, bonds, commodities, currencies, etc. – rely on both investor sentiment and the state of underlying economic factors. At the best of times, the interplay of these two forces makes it challenging to make forecasts. However, 2023 was an exceptionally tough one for investors to navigate, given a couple of not-so-common factors.

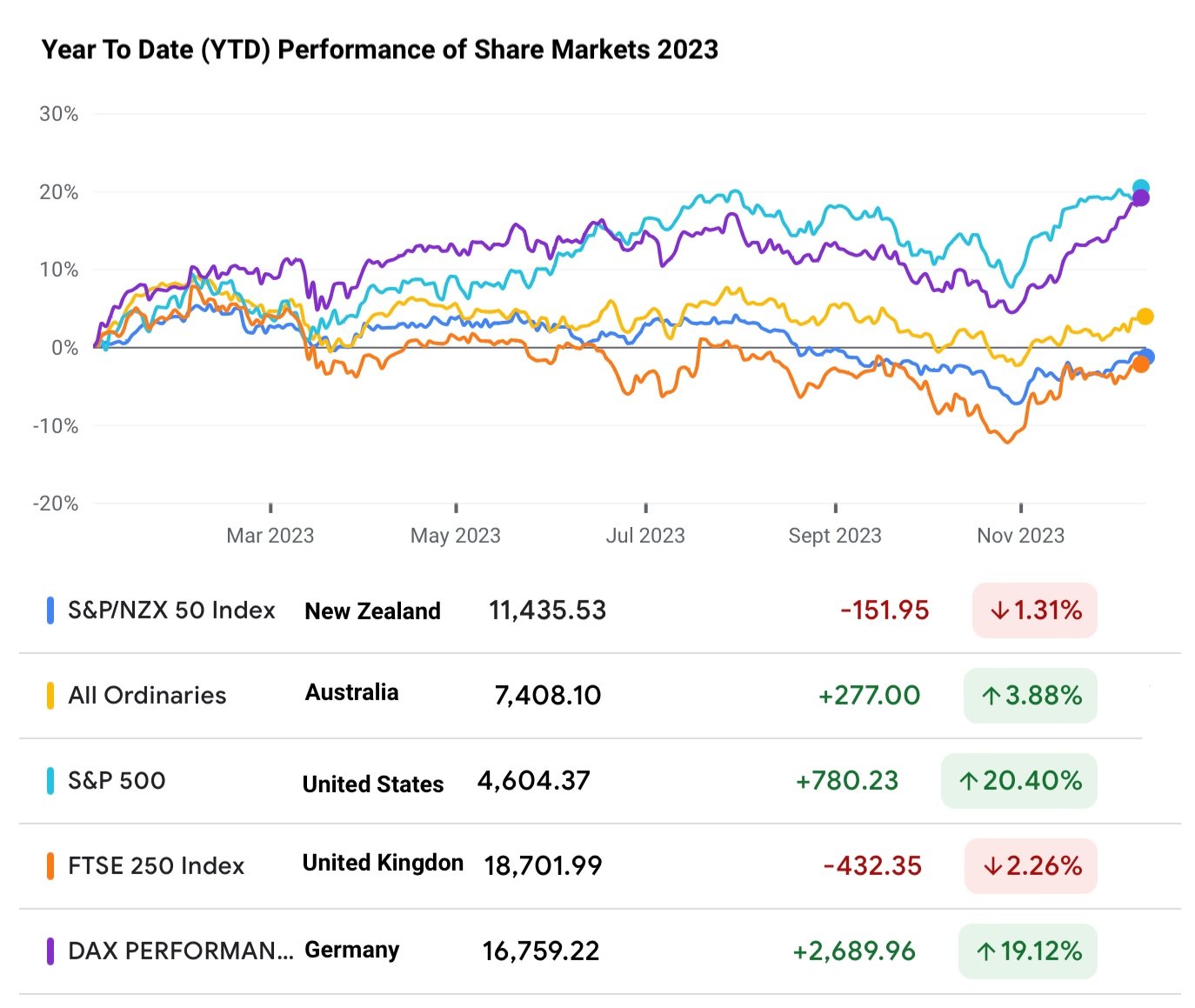

Dated 11 December 2023. Chart courtesy Google Finance- Link here

For starters, consumer demand was hard to predict as the world emerged out of pandemic-driven lockdowns. But, in general, consumers emerged from the lockdowns with very high levels of savings, from either spending less through the lockdowns or receiving government aid and subsidies. As such, the pent-up demand on goods and services put pressure on their supply. As a direct result, prices skyrocketed and inflation surged – across the globe. This pattern of demand-supply dynamics has been unusual compared to the past many decades, not surprisingly given the occurrence of the pandemic being a once-in-a-hundred-year-or-so event.

In response to heightened inflationary pressures, most central banks were forced to raise interest rates (meaning, the cost to borrow money). As a bit of context, most central banks have a mandate to limit inflation to 2%. To cite some examples, by 2022, inflation in the US was over 8%, in the UK over 11% and in NZ over 7%, approximately – well above their mandated levels. Most countries fared similarly in the immediate aftermath of the pandemic. The hike in interest rates was a natural response to this level of inflationary pressure, increasing the cost of borrowing money and curtailing spending.

However, the above interest rate hike must be put in context to understand its implications on investment markets. In 2020, the headline interest rate in the US was a smidgen over 0%. Today, it stands at about 5.5% – a 22 year high. Similarly in the UK, the central bank has raised interest rates 14 times over the last couple of years to 5.25%. Closer to home, the trend is similar at 5.5% today – the last time it was higher was in 2009.

An increase in the cost of borrowing money impacts both consumers and businesses, constraining their ability to spend and stoking the cost of living crisis. However, overdoing the hikes will lead to a recession with the risk of both business activity and consumer spending coming to a stall.

Achieving this balance between constraint and stimulus has never been trickier when considering the mix of current geo-political issues in the Middle East and Ukraine as well as economic shifts in China with upheavals in its domestic property sector. All of these factors impact on both investor sentiment and economic fundamentals.

On the bright side, it does appear that sustained rate hikes are taking effect, which is signalling a slowdown or at least a pause in hikes, if not cuts. Although multiple factors continue to hang in the balance, the expectation now is that 2024 will see a slowdown (rather than a full blown recession).

Through such uncertain times it becomes all the more important to be disciplined in how you manage your investment portfolio. If you designed your portfolio appropriately (i.e., assigned the optimal allocation to different assets) then it is worth monitoring it regularly. This is to ensure that the investment thesis it was originally built on hasn’t changed.

Regular monitoring also helps in knowing when to tweak those allocations (if needed), rather than risk chopping and changing them based on short-term trends in the market and other peoples’ sentiment-driven actions.

2023 has been a tough year – even for Santa to decide whether markets have been naughty or nice! But, as the saying goes, fortune favours those who are prepared.